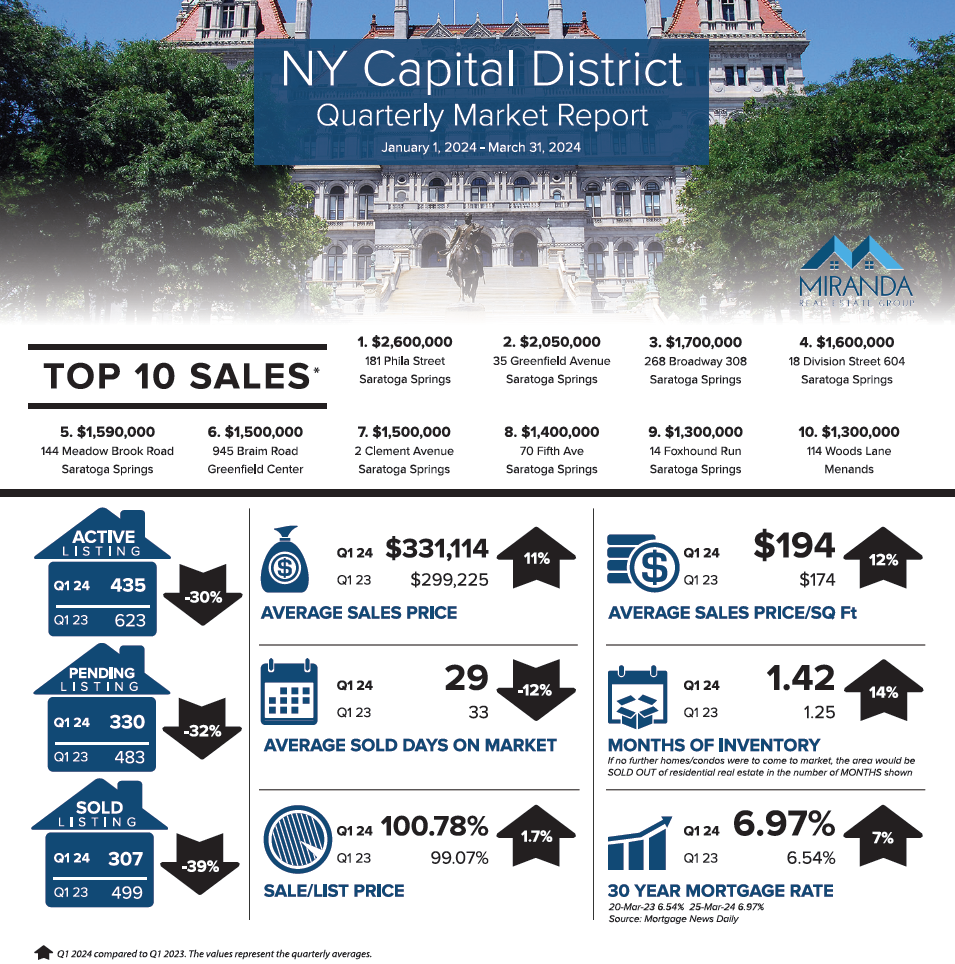

- Average sales price was up 11%.

- The inventory of homes available for sale remained relatively flat. Active listings were down 30%, which was offset by fewer closed sales (due to the lack of available inventory).

- Volume of closed sales was down 39%, and pending sales were down 32%.

- Interest rates are up ~.5% compared to ’23.

- Inventory remains challenging, sitting at a ~1.5 months supply of homes for sale.

Inventory levels of a 4 – 6 months’ supply is considered balanced, so there is still a long way to go.